How Regulation Shapes South Korea's Fintech Landscape: 2026 Insights

WRITTEN BY

Dylan Coombs

Citcon

Commercial Leader

Date

Jun 8, 2026

Subscribe to our interesting updates

SHARE ON

Regulation in South Korea's fintech ecosystem is a critical factor shaping its trajectory. By 2026, the fintech market in Korea is expected to grow by 15%, highlighting the importance of regulatory frameworks in facilitating innovation and protecting consumers.

The South Korean fintech sector is experiencing rapid growth, driven by technological advancements and a supportive regulatory environment. According to Statista, the fintech market in South Korea was valued at USD 11.5 billion in 2023, with projections to reach USD 13.2 billion by 2026. Simultaneously, a report by the Bank of Korea in 2022 indicated a 25% increase in mobile payment transactions, showcasing consumer adoption. These trends underscore the need for a robust regulatory framework to ensure sustainable growth and innovation.

South Korea's regulatory landscape is characterized by its dynamic approach to fintech innovation. The Financial Services Commission (FSC) plays a pivotal role, implementing policies that encourage technological advancements while safeguarding consumer interests. In 2025, the FSC introduced new guidelines for digital banking, enhancing security measures and compliance standards. Additionally, the Korea Financial Telecommunications & Clearings Institute (KFTC) reported a 30% increase in the adoption of open banking platforms in 2024, further illustrating the impact of regulatory support.

South Korea's Fintech Market Dynamics

South Korea's fintech market is shaped by several key dynamics, including regulatory frameworks, consumer behavior, and technological advancements. The FSC's proactive stance has facilitated a 40% increase in fintech startups from 2023 to 2026, according to KPMG. Meanwhile, consumer demand for digital wallets like KakaoPay and Naver Pay has surged, with a 78% penetration rate reported by Euromonitor in 2024. These factors create a fertile environment for fintech innovation.

The regulatory environment has also fostered a competitive market landscape. A report by Deloitte in 2025 found that 68% of South Korean consumers prefer digital payment solutions over traditional banking methods, driven by convenience and security. Furthermore, the introduction of the Digital Financial Innovation Act in 2024 has streamlined compliance processes, enabling fintech firms to bring products to market faster.

- Fintech market size: USD 13.2 billion by 2026 (Statista, 2023).

- Mobile payment growth: 25% increase in 2022 (Bank of Korea).

- Digital wallet penetration: 78% in 2024 (Euromonitor).

- Startup growth: 40% increase from 2023 to 2026 (KPMG).

Challenges in Regulatory Compliance

Despite the supportive regulatory environment, challenges persist, particularly in compliance. A fintech startup in Seoul, for instance, faced hurdles in meeting the stringent KYC requirements introduced in 2025. According to a report by PwC, 35% of fintech firms in 2024 struggled with compliance costs, impacting their operational efficiency. These challenges highlight the need for streamlined regulatory processes to foster innovation without compromising security.

Moreover, the evolving nature of fintech technologies presents regulatory challenges. The rapid adoption of blockchain and AI technologies requires continuous updates to regulatory frameworks. The FSC's 2026 guidelines for AI-driven financial services aim to address these challenges, but implementation remains complex.

How Regulatory Compliance Works: Step-by-Step

Understanding regulatory compliance in South Korea involves several key steps:

- Step 1: Conduct a comprehensive risk assessment to identify potential compliance gaps.

- Step 2: Develop a robust KYC process in line with the 2025 guidelines.

- Step 3: Implement data protection measures to safeguard consumer information.

- Step 4: Regularly review and update compliance protocols to align with evolving regulations.

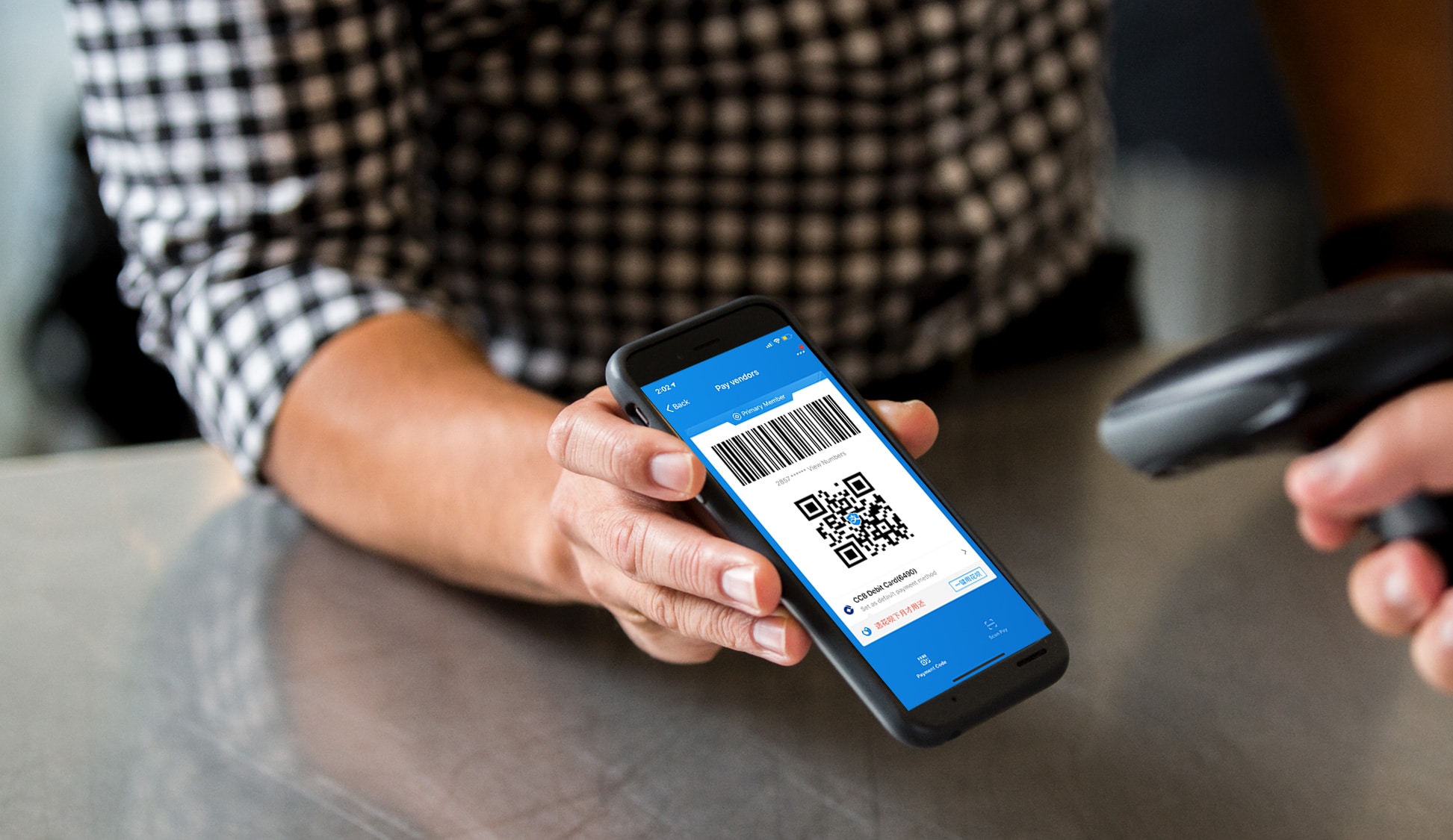

In-Depth: South Korea's Payment Methods

South Korea's payment landscape is diverse, driven by consumer preferences and technological advancements. Popular methods include KakaoPay, Naver Pay, Toss, and Samsung Pay. According to the KFTC, KakaoPay saw a 50% increase in user transactions in 2025, while Toss reported a 30% growth in its user base. These platforms offer seamless integration with digital banking services, enhancing consumer convenience.

Regulatory bodies like the FSC have played a crucial role in shaping the payment ecosystem. The introduction of the Open Banking system in 2024 facilitated a 20% increase in cross-platform transactions, as reported by the Bank of Korea. This integration has enabled consumers to access multiple financial services through a single platform.

- KakaoPay growth: 50% increase in 2025 (KFTC).

- Toss user growth: 30% in 2025.

- Open Banking impact: 20% increase in transactions (Bank of Korea, 2024).

The Business Case: ROI and Cost Analysis

For fintech firms, understanding the ROI and cost implications of regulatory compliance is crucial. A study by Bain & Company in 2025 found that companies adhering to compliance standards saw a 15% increase in consumer trust and a 10% reduction in operational risks. Additionally, firms that integrated digital payment solutions reported a 25% revenue uplift, as highlighted by McKinsey & Company in 2024. The cost of non-compliance, on the other hand, can be significant, with potential fines and reputational damage.

- Consumer trust increase: 15% with compliance (Bain & Company, 2025).

- Revenue uplift: 25% with digital payments (McKinsey, 2024).

- Risk reduction: 10% through compliance.

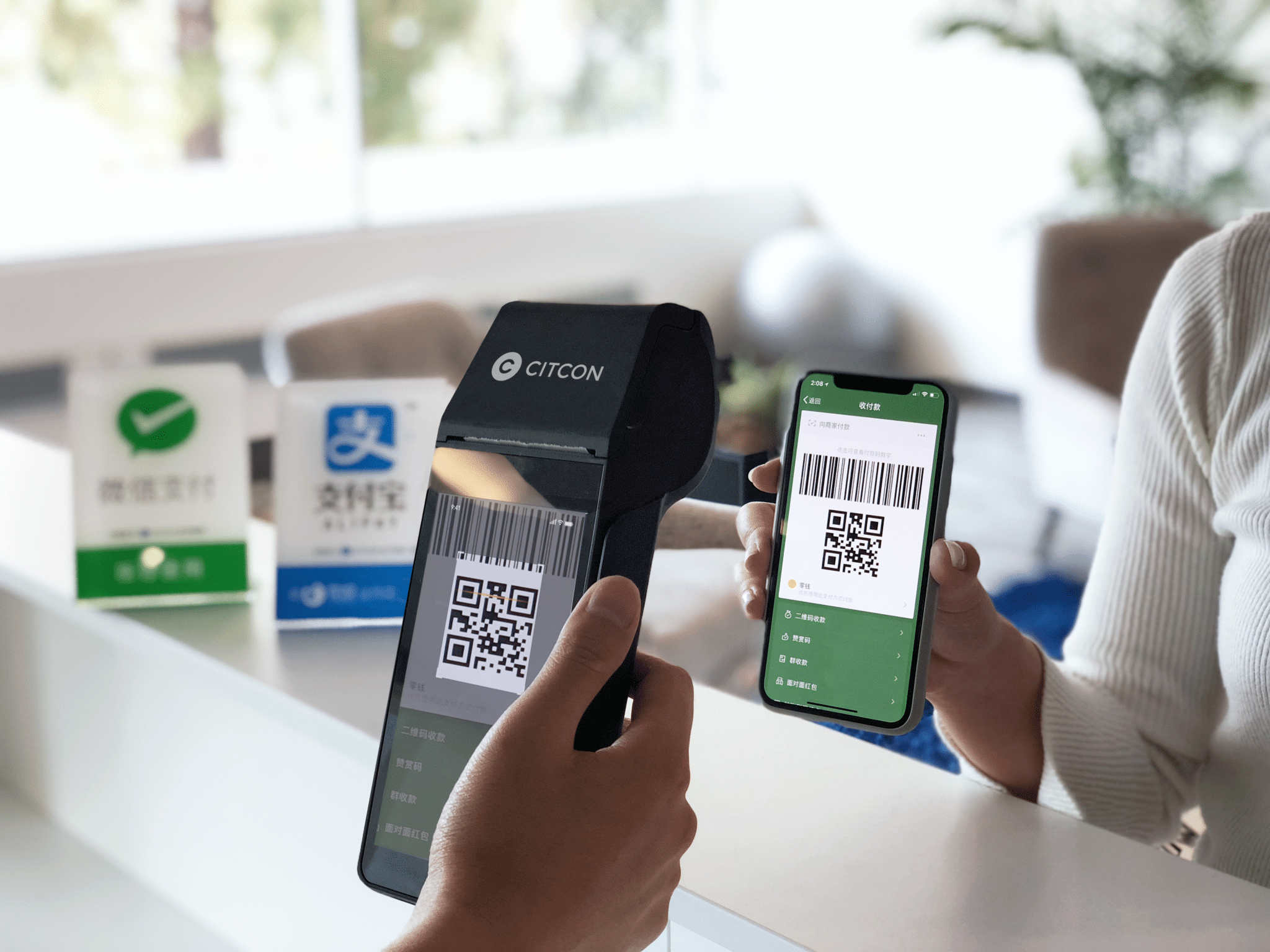

Optimizing Compliance with Citcon

Citcon offers a comprehensive solution for fintech firms navigating South Korea's regulatory landscape. With a single API, businesses can access over 100 payment methods, including popular APAC wallets like KakaoPay and Naver Pay. Citcon's platform supports rapid deployment, allowing integration within days, not months. Additionally, Citcon provides dedicated account management and volume-rate negotiation, ensuring cost-effective compliance with PCI-DSS Level 1 standards. This approach addresses the compliance challenges faced by fintech firms, enabling them to focus on innovation and growth.

What are the costs associated with fintech compliance in South Korea?

Compliance costs in South Korea can vary significantly, but a report by Deloitte in 2024 estimated that fintech firms spend approximately 8-10% of their revenue on regulatory compliance. This includes costs related to KYC, data protection, and adherence to financial regulations.

How long does it take to integrate a digital payment solution in South Korea?

Integrating a digital payment solution in South Korea typically takes 2 to 3 months. However, with Citcon's platform, businesses can achieve integration within days, thanks to its streamlined API and support for multiple payment methods.

What technical requirements are necessary for fintech compliance?

Fintech compliance in South Korea requires robust KYC processes, data protection measures, and adherence to financial regulations. Firms must implement secure data encryption and regularly update their compliance protocols to meet evolving standards.

What is the ROI for implementing digital payment solutions?

Implementing digital payment solutions can yield a significant ROI. According to McKinsey & Company in 2024, fintech firms reported a 25% revenue uplift after integrating digital payment systems, driven by increased consumer trust and transaction efficiency.

How does South Korea's fintech regulation compare to other countries?

South Korea's fintech regulation is considered progressive, with a focus on fostering innovation while ensuring consumer protection. The FSC's proactive approach has facilitated fintech growth, making it a leading market in the APAC region, comparable to Singapore's regulatory framework.

What are common objections to fintech compliance?

Common objections to fintech compliance include concerns about high costs, complex regulatory requirements, and the potential impact on innovation. However, compliance is essential for consumer trust and long-term sustainability.

Key Takeaways

- Fintech market growth: Expected to reach USD 13.2 billion by 2026, highlighting significant opportunities.

- Regulatory impact: The FSC's guidelines have facilitated a 40% increase in fintech startups from 2023 to 2026.

- Consumer adoption: Mobile payment transactions increased by 25% in 2022, showcasing rapid adoption.

- Compliance ROI: Firms adhering to compliance standards saw a 15% increase in consumer trust.

- Payment method diversity: KakaoPay and Naver Pay dominate with 78% penetration in 2024.

.jpg)

.png)