How to Choose Online Payment Services in 2025

WRITTEN BY

Dylan Coombs

Citcon

Commercial Leader

Date

Oct 10, 2025

Subscribe to our interesting updates

SHARE ON

By 2025, online shoppers expect to pay with their favorite wallet, buy now pay later (BNPL) plan, or local card in a few taps no matter where the merchant is located. If they cannot, they abandon quickly. Baymard Institute still pegs the average global cart-abandonment rate at 70 percent, and lack of preferred payment methods is one of the top three reasons. Selecting the right online payment service has therefore moved from a back-office decision to a growth lever your executive team should own.

Why your choice of payment service matters more than ever

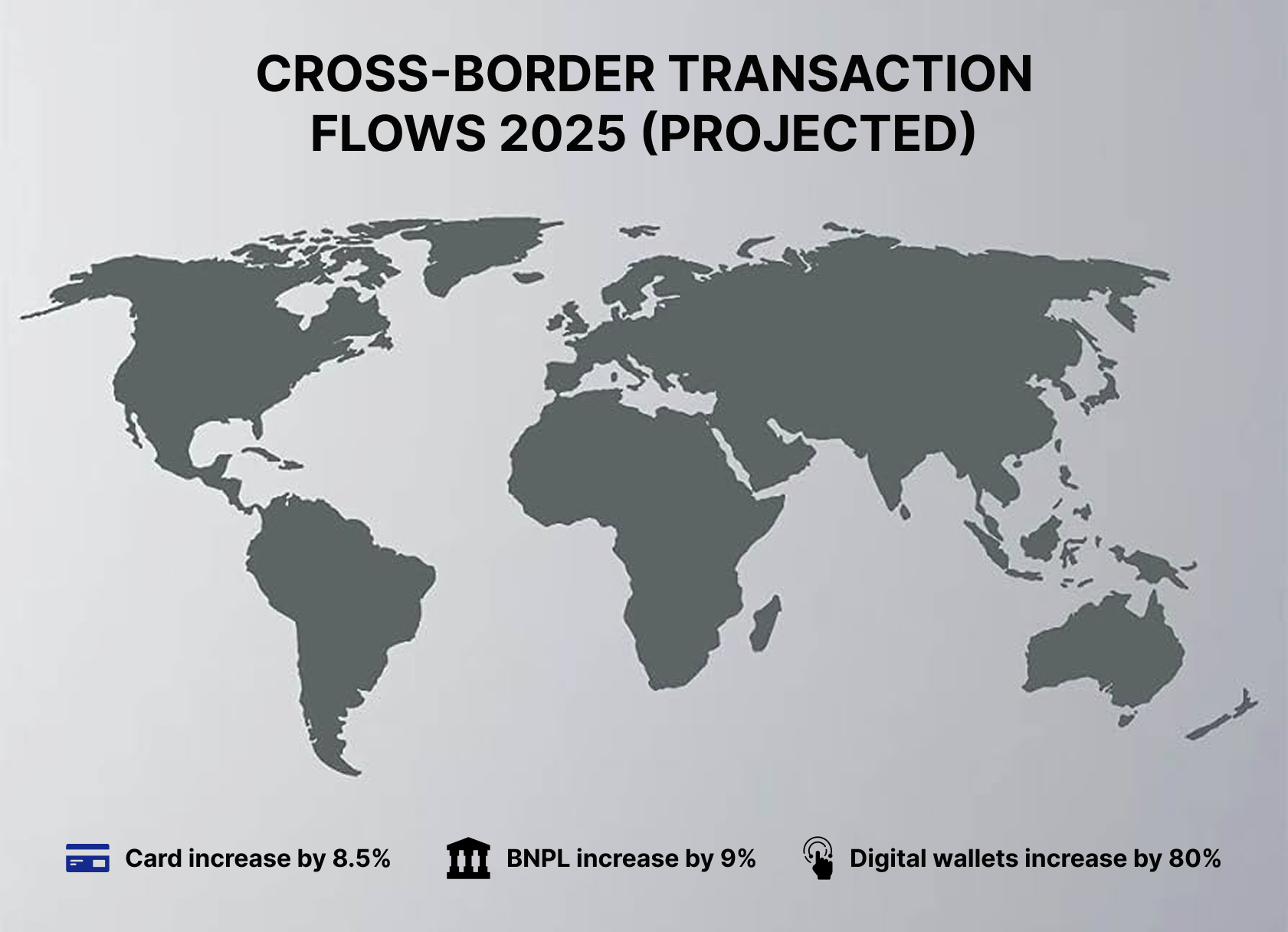

1. Cross-border growth is accelerating. eMarketer projects retail eCommerce sales to surpass 8.5 trillion USD by 2026, with almost two-thirds of that volume crossing at least one border.

2. Local and alternative payment methods dominate. McKinsey’s 2024 Global Payments Report shows digital wallets already account for 54 percent of global eCommerce spend and will hit 63 percent by 2027.

3. Compliance is complex. PSD3 in Europe, the U.S. FedNow rollout, and dozens of data-privacy laws make it harder to stay compliant on your own.

4. Checkout experience drives conversion. Adyen’s 2025 Retail Report found that 62 percent of consumers drop off if checkout feels unfamiliar.

10 key decision factors when comparing online payment services

1. Customer payment preferences

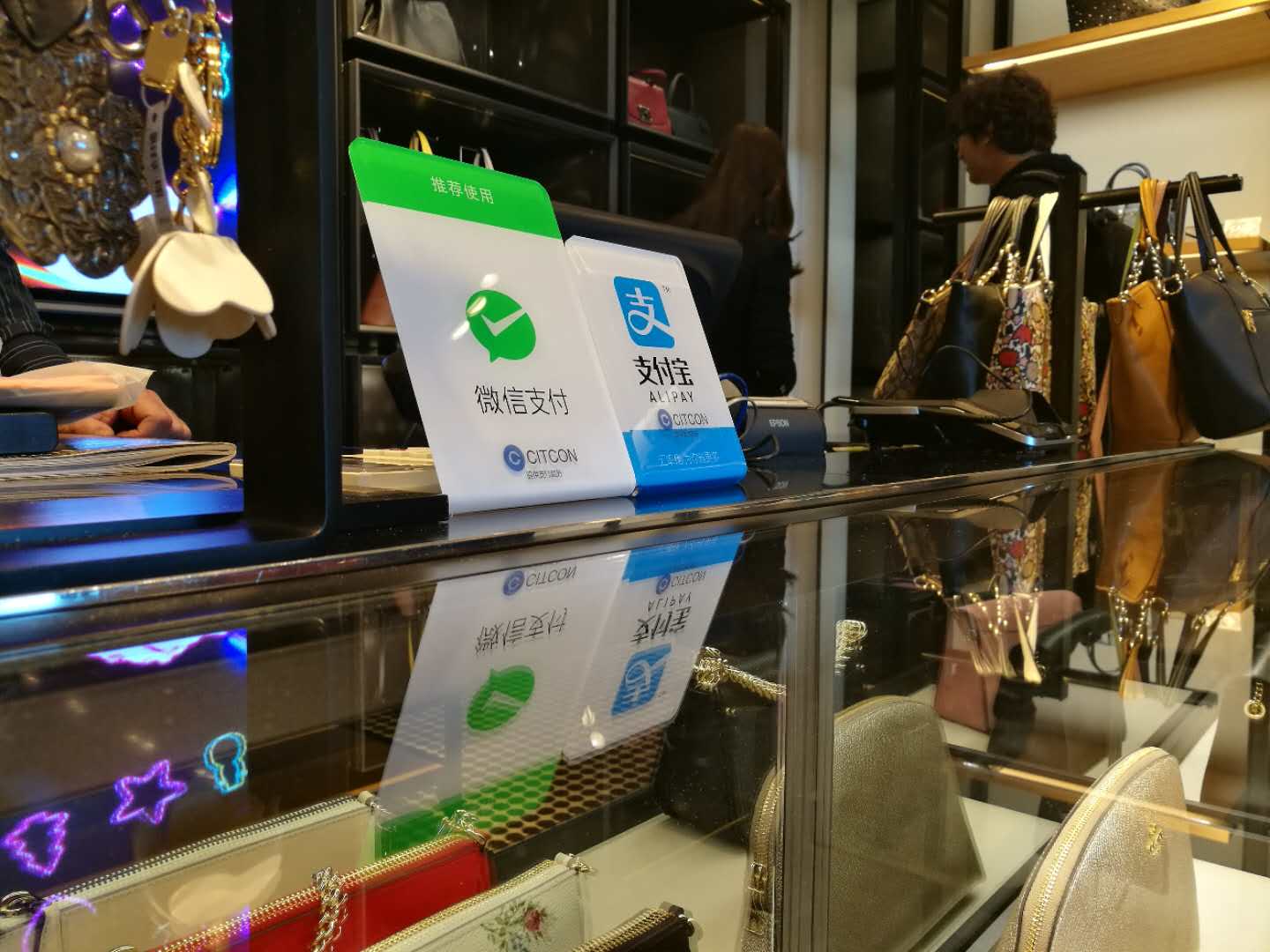

Match the mix of cards, wallets, BNPL, and domestic schemes your target shoppers actually use. Offering Alipay to U.K. buyers adds little value, but it is critical if you serve Chinese tourists or students. Citcon, for example, supports 100+ methods in a single integration, including Alipay, WeChat Pay, PayPal, Afterpay, and major card brands.

2. Global reach and local currency settlement

If you plan to expand, verify the provider can process in all target markets and settle funds in the currencies you need. Dual-currency or dual-pricing features can help you meet card-surcharge rules while showing transparent prices to shoppers.

3. Cost structure transparency

Compare:

- Per-transaction fees, interchange, scheme fees

- FX mark-ups for cross-border transactions

- Chargeback and dispute fees

- Monthly SaaS or gateway fees

Hidden FX can erase margin gains, so negotiate blended or interchange-plus pricing and insist on line-item reporting.

4. Security, compliance, and risk tools

Look for PCI-DSS Level 1 certification, point-to-point encryption (P2PE), tokenization, and built-in fraud tools that use machine learning. Automated KYC and sanctions screening lower onboarding friction while meeting AML laws.

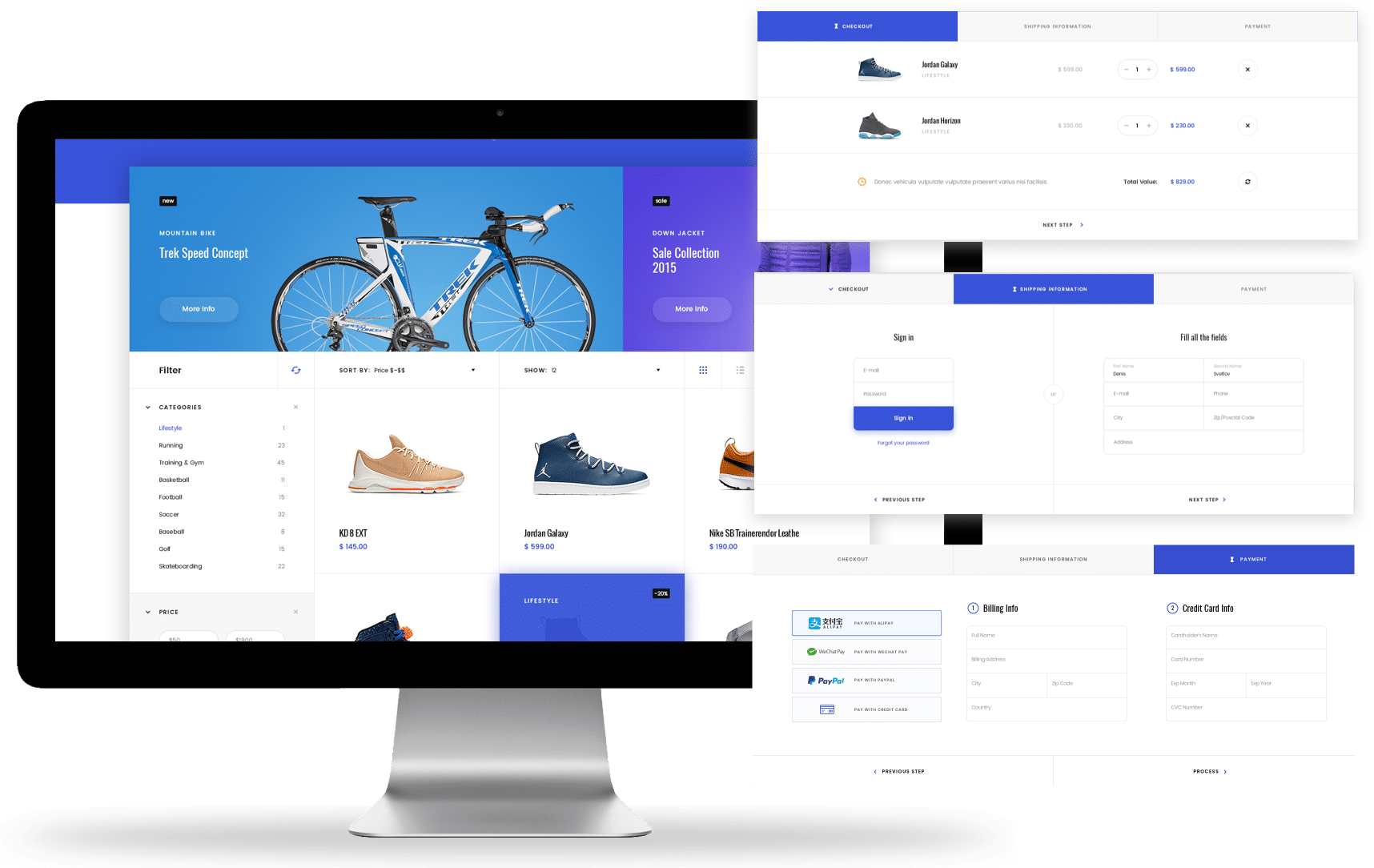

5. Developer experience and time to market

A modern RESTful API, SDKs, and clear documentation shorten integration cycles. Ask how long a typical merchant takes to go live. Citcon merchants often deploy in weeks thanks to a single API and pre-built plugins.

6. Settlement speed and working-capital impact

Standard card settlement can take T+3 days or longer. Some providers now offer T+1 or even same-day funding for qualifying businesses. Faster settlement reduces reliance on short-term credit.

7. Reporting, reconciliation, and analytics

Consolidated, exportable reports save finance teams hours of manual work. Automated reconciliation was once a nice-to-have; in 2025 it is table stakes.

8. Multi-channel capabilities

Unified commerce means supporting the same payment methods online, in-app, and in-store. QR code acceptance, payment links, and pay-by-SMS make omnichannel promotions seamless. Our article on how mobile payment systems work dives deeper into channel options.

9. Value-added features

Token-on-file, recurring billing, BNPL orchestration, marketing add-ons (loyalty coupons, wallet-based follow features) can lift lifetime value and AOV. Evaluate roadmap alignment with your growth plans.

10. Support quality and service-level agreements (SLAs)

24×7 support, dedicated account management, and a published uptime guarantee minimize revenue loss during outages.

2025 trends shaping payment strategy

1. Super-app dominance. Wallets like Alipay+, PayPay, and GrabPay bundle payments, loyalty, and lending, creating “one-tap” checkout experiences.

2. AI-driven fraud defense. Real-time behavioral biometrics reduce false positives by up to 40 percent, per Juniper Research 2025 data.

3. Central bank digital currency (CBDC) pilots. China’s e-CNY and Europe’s digital euro may reach limited commercial rollouts this year, so ask providers about CBDC-readiness.

4. Sustainable payments. Carbon-neutral payment processing is a buying criterion for 31 percent of Gen Z shoppers, according to Deloitte’s 2025 Consumer Survey.

5. Dual-pricing compliance. Several U.S. states now require clear disclosure of card surcharges; providers with built-in dual-pricing help merchants stay compliant.

A practical framework to select your provider

1. Map your customer journeys. List the countries, channels, and devices involved in each purchase path.

2. Identify must-have payment methods per market. Use internal analytics and resources like local central-bank surveys.

3. Short-list providers that cover at least 90 percent of required methods.

4. Score each vendor across the 10 factors above on a 1–5 scale. Weight factors based on your strategy (for example, weight “global reach” higher if expansion is urgent).

5. Run a sandbox test. Process sample payments, refunds, and chargebacks. Validate webhook reliability and data exports.

6. Request merchant references in your vertical and region. Ask specifically about downtime, support responsiveness, and hidden fees.

7. Negotiate a pilot period with exit clauses. Prefer monthly SaaS over long-term lock-ins while you validate performance.

Following this framework reduces selection time from months to weeks and aligns stakeholders across product, finance, and compliance.

Common pitfalls (and how to avoid them)

- Focusing only on headline transaction fees while ignoring FX and exemption fees.

- Integrating multiple gateways per region, which increases maintenance overhead. A single-API model like Citcon’s lowers tech debt.

- Forgetting post-purchase flows. Refund speed and dispute handling impact CSAT just as much as checkout UX. See our guide on reducing chargebacks.

- Assuming one provider will automatically activate every payment method. Regulatory approvals may require additional KYC.

Quick 2025 checklist for payment-service selection

☐ Supports all target wallets, BNPL options, and cards

☐ Compliant with PCI-DSS, PSD3, and local data-privacy laws

☐ Offers unified API and SDKs for web, iOS, Android

☐ Provides daily settlement in required currencies

☐ Includes automated reconciliation and real-time reporting

☐ Delivers 99.9 percent or higher uptime SLA

☐ Transparent fee schedule with no hidden mark-ups

☐ 24×7 multilingual support

Frequently Asked Questions

What are alternative payment methods? Alternative payment methods (APMs) include any non-card option such as digital wallets, BNPL plans, bank transfers, and domestic card schemes. Our full primer on APMs is available here.

How much do online payment services cost? Costs vary by region and method. Expect 2.5–4 percent for international cards, 0.8–2 percent for wallets, and lower flat fees for local bank schemes. Always confirm FX mark-ups and chargeback fees.

Is a single provider enough for global expansion? Often yes. Platforms that aggregate 100+ payment methods through one API can cover 90 percent of global transaction volume. Some merchants still keep a regional backup for redundancy.

How can I reduce fraud without hurting conversion? Use layered defense: device fingerprinting, behavioral analytics, 3-D Secure 2, and real-time risk scoring. Many modern gateways bundle these tools or integrate with specialist providers.

When should I add BNPL? If your AOV is above 100 USD or you sell to Gen Z/Millennial shoppers, BNPL can boost conversion. Ensure your gateway supports your preferred BNPL providers and handles reconciliation automatically.

Ready to simplify global payments?

Choosing the right online payment service in 2025 is critical to revenue growth, customer trust, and operational efficiency. If you want to launch 100+ payment methods through a single API, accelerate time to market, and cut back-office costs, request a personalized demo of Citcon’s unified global payment platform today.

.jpg)

.png)