China Cross-Border Payments: How to Accept Alipay, WeChat Pay & UnionPay and Send Payouts

WRITTEN BY

Dylan Coombs

Citcon

Commercial Leader

Date

Apr 23, 2026

Subscribe to our interesting updates

SHARE ON

.jpg)

China's Payment Market: Alipay, WeChat Pay & UnionPay by the Numbers

No payment market on earth moves faster, or at greater scale, than China's. The country has effectively leapfrogged card-based infrastructure entirely, building a mobile-first financial system that processes transactions worth trillions of dollars annually. According to data from the People's Bank of China, the country's non-cash payment volume has exceeded $100 trillion USD — a figure that dwarfs comparable markets in North America and Europe. Mobile payment penetration in China now sits above 86% of the adult population (Statista, 2024), making cash and physical cards largely irrelevant in daily commerce.

For global merchants — whether you operate luxury retail in New York, hospitality brands across North America, or e-commerce platforms serving international buyers — China is not a future opportunity. It is a present reality. Chinese consumers traveling abroad, purchasing cross-border, or receiving payouts from international platforms expect to transact in the digital wallets they use at home. Businesses that cannot meet that expectation leave revenue on the table. Those that build the right payment infrastructure now are positioning themselves for compounding advantage.

Understanding the China Payment Ecosystem: Alipay, WeChat Pay, and UnionPay

Three platforms form the backbone of Chinese consumer payment processing — and understanding each is essential before evaluating any cross-border solution.

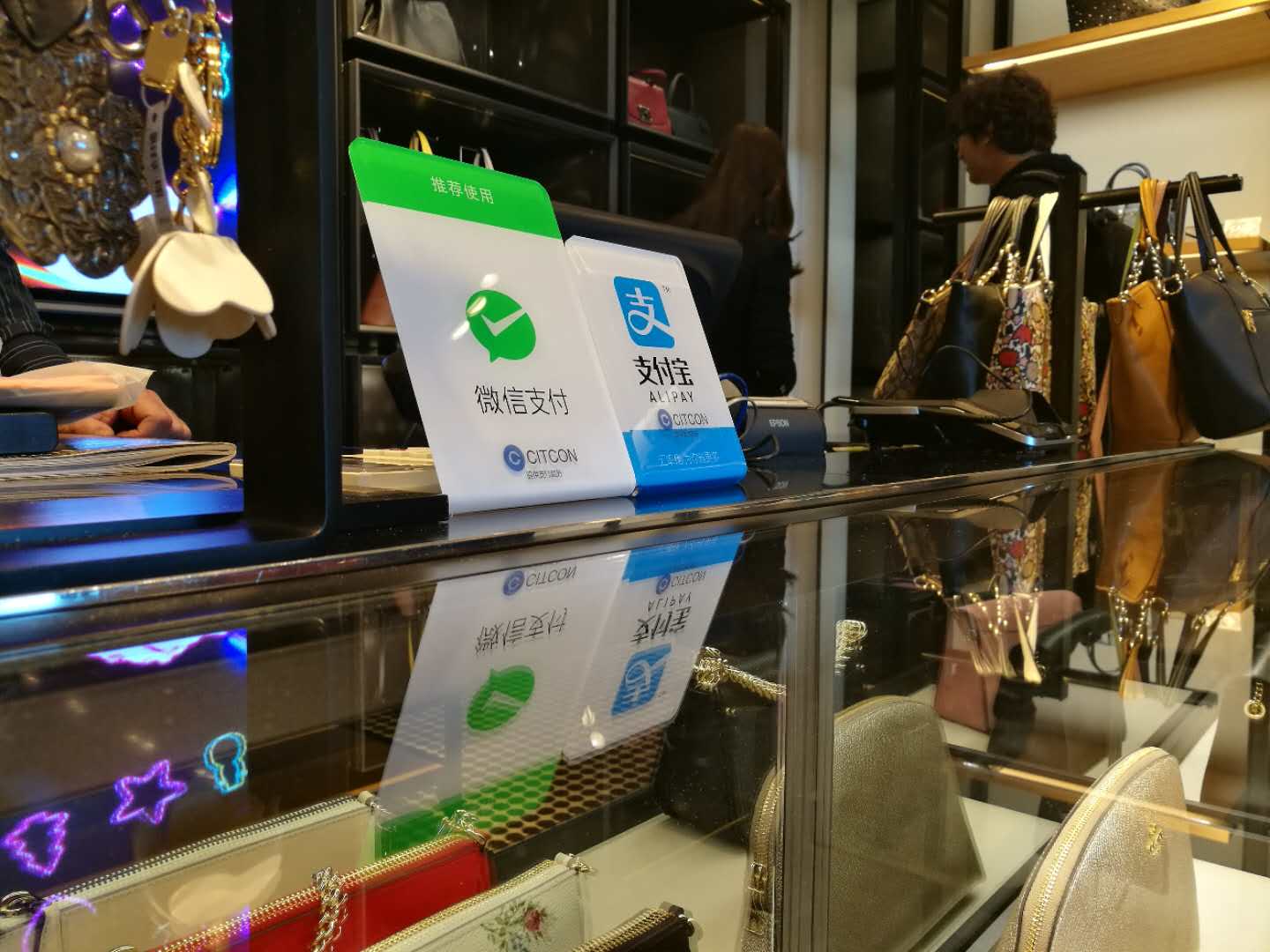

Alipay (Ant Group)

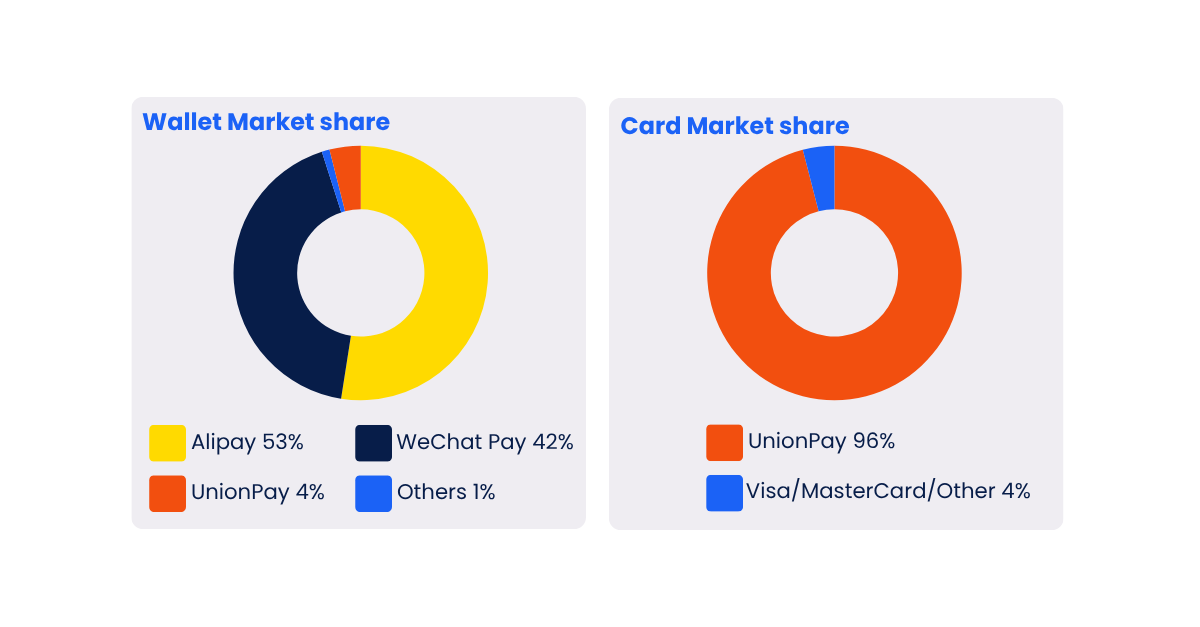

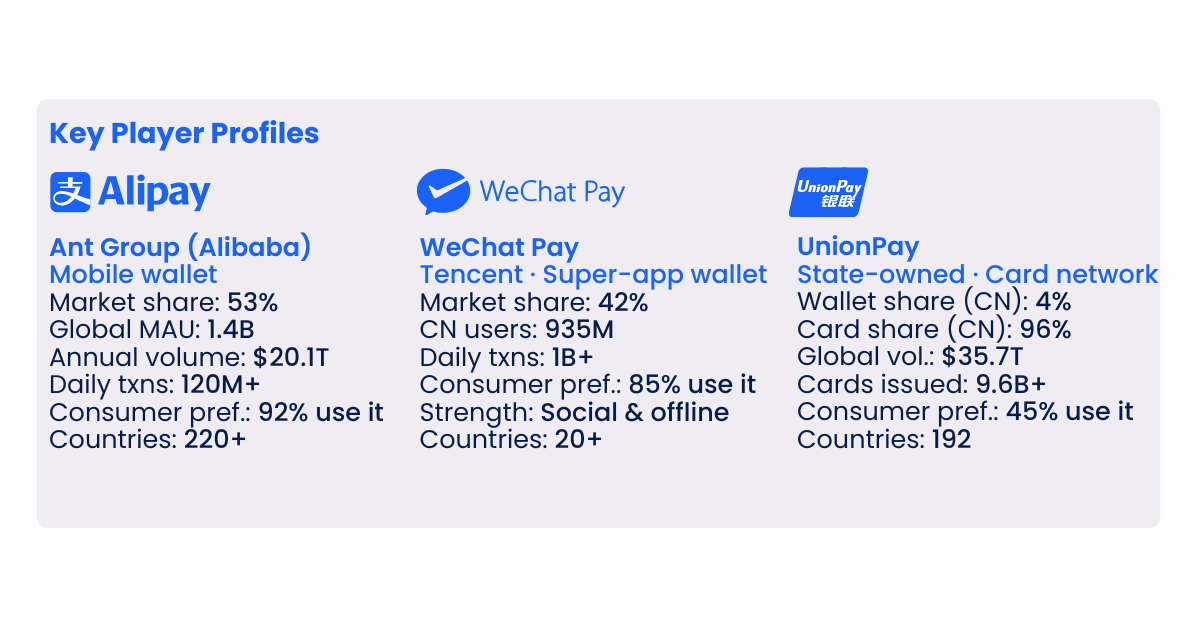

Alipay, operated by Ant Group (an affiliate of Alibaba), is one of the world's largest digital payment platforms. With over 1.3 billion annual active users globally (Ant Group, 2024), Alipay commands a dominant share of China's mobile wallet market. Beyond domestic transactions, Alipay has aggressively expanded its international footprint through Alipay+, a cross-border payment and marketing solution that connects overseas merchants directly to Chinese consumers traveling or spending abroad. For US merchants evaluating Alipay merchant integration, Alipay+ is the primary bridge — enabling acceptance without requiring separate domestic Chinese licensing.

WeChat Pay (Tencent)

WeChat Pay is embedded inside WeChat — China's dominant super-app used by 1.4 billion monthly active users for messaging, social media, and commerce (Tencent, Q4 2024). WeChat Pay processes over 1 billion commercial transactions per day, with more than 935 million individuals using the payment feature monthly. WeChat accounts for 35% of all mobile usage time in China, meaning payment and commerce are inseparable from daily digital life. WeChat Pay now operates across 49 countries in 16 major currencies. Tencent's FinTech segment generated approximately $14 billion USD in revenue in 2024 — a 24% year-on-year gross profit increase — underscoring the platform's sustained commercial dominance.

UnionPay (银联)

UnionPay rounds out the picture as China's state-backed card network and digital wallet infrastructure provider. With over 500 million registered UnionPay app users and 400+ wallet partners in China alone, UnionPay functions as the essential card rail and digital wallet network for Chinese consumers who prefer bank-linked payment options. As a China UnionPay payment gateway solution, it extends across 200+ regions globally. For merchants, connecting to UnionPay enables access to a high-value, mobile-first consumer base that seeks out familiar, secure payment experiences when spending internationally.

Together, these three platforms represent the near-total landscape of Chinese consumer payment infrastructure. No serious cross-border payment strategy targeting Chinese consumers — whether for payment acceptance or payout disbursement — can afford to treat any one of them as optional.

China Cross-Border Payout Challenges: Fragmentation, Speed & Compliance

Understanding the market is straightforward. Executing within it is significantly harder. Merchants and enterprise finance teams who attempt to engage China's payment rails directly encounter a set of structural obstacles that are, without the right infrastructure partner, genuinely costly to navigate.

Fragmentation: Alipay, WeChat Pay, and UnionPay are separate platforms with separate APIs, compliance requirements, and onboarding processes. A business attempting to settle payments in China or disburse payouts to China-based recipients independently must manage three distinct integrations, three sets of technical documentation, and three ongoing merchant relationships. The operational overhead is real — and it scales poorly.

Speed Expectations: Chinese consumers and business partners operating in an ecosystem where payments settle in seconds have little tolerance for the multi-day clearing windows common in legacy cross-border payment infrastructure. For platforms disbursing earnings to China-based sellers or creators, payout delays erode trust and retention. Speed is a competitive differentiator, not a bonus feature.

Regulatory and Compliance Complexity: Cross-border payments involving the Chinese renminbi (RMB) are subject to PBOC oversight, foreign exchange controls, and evolving compliance frameworks that vary depending on the payment rail, transaction type, and counterparty. For enterprise finance teams unfamiliar with these frameworks, navigating RMB settlement for merchants without experienced infrastructure support introduces meaningful compliance and operational risk.

FX and Settlement Friction: Converting currencies at the point of payout, managing exchange rate exposure across multiple wallets, and ensuring settlement accuracy in RMB — all while maintaining audit trails for compliance purposes — requires infrastructure that most merchants simply do not have in-house.

These are not niche problems. They are the defining operational challenges for any business that transacts at scale with Chinese consumers or counterparties.

How Citcon Solves China Cross-Border Payments: One Platform, Complete Coverage

Citcon's cross-border payment platform is purpose-built to eliminate exactly these obstacles. Where other solutions address one wallet or one use case, Citcon delivers unified access to Alipay, WeChat Pay, and UnionPay through a single API integration — removing the need for redundant onboarding, separate compliance management, or duplicated technical work.

For US and North American merchants seeking Alipay+ integration or WeChat Pay acceptance in North America, Citcon provides certified, direct connectivity to both platforms. One integration activates the full spectrum of Chinese mobile payment acceptance — in-store, online, and in-app.

On the payout side, Citcon's platform functions as a true China cross-border payout solution. Whether you are disbursing earnings to China-based marketplace sellers, remitting funds to Chinese supplier partners, or settling platform revenues in RMB, Citcon's infrastructure handles the complexity — fast, compliant, and operationally clean. The platform supports RMB settlement for merchants operating under cross-border payment frameworks, with FX handling integrated into the settlement process to reduce exposure and simplify reconciliation.

Speed is not incidental to Citcon's architecture — it is central. Cross-border payouts to China execute at a pace that meets the expectations of Chinese counterparties accustomed to near-instant domestic settlement. For platforms competing on trust and reliability, this matters enormously.

Citcon's international mobile wallet payout capabilities are not limited to China alone. The same unified platform that delivers China connectivity also supports a broader cross-border payment gateway across Asia — enabling merchants to scale their international payment acceptance without rebuilding infrastructure for each new market.

Which Businesses Need a China Cross-Border Payment Gateway?

Citcon's China payment capabilities deliver the highest return for businesses operating in specific, high-impact verticals.

Retailers and Hospitality Brands serving Chinese tourists benefit immediately from in-store and in-app acceptance of Alipay, WeChat Pay, and UnionPay. A Chinese tourist payment solution is not a courtesy — research consistently shows that Chinese travelers spend significantly more when they can pay using their preferred wallets (McKinsey, 2023). Not accepting Chinese mobile payments is not a partial sale. It is no sale.

E-Commerce Platforms and Marketplaces with China-based suppliers or seller communities benefit from Citcon's payout infrastructure. Disbursing earnings in RMB, at speed, through wallets that recipients actually use, reduces friction and improves platform retention.

Enterprise Finance Teams managing recurring cross-border settlements to China need a partner with proven compliance infrastructure, reliable FX handling, and a single reconciliation layer — not three separate vendor relationships. Citcon delivers that consolidation.

Platform Operators in media, creator economy, or digital services disbursing to Chinese creators or contributors need international mobile wallet payouts that are fast, auditable, and compliant. Citcon's infrastructure is built for exactly this use case.

Why Accept Chinese Mobile Payments Now: The Business Case

China's payment ecosystem will not stand still. Alipay+ continues to expand its global merchant network. WeChat Pay is deepening its cross-border capabilities across new markets. UnionPay's digital wallet partnerships now extend to over 200 regions worldwide. As Chinese outbound tourism and cross-border commerce continue their recovery and growth, the volume of Chinese consumer spending flowing through international merchants will only increase.

Businesses that establish their China payment and payout infrastructure now — before competitive pressure makes it urgent — gain the operational maturity, technical reliability, and consumer trust that late movers cannot replicate quickly. Every month without a compliant, unified China cross-border payment gateway solution is a month of friction, missed transactions, and payout delays that erode relationships and revenue.

Citcon has built the infrastructure. The wallets are connected. The compliance frameworks are in place.

Contact our payment professionals TODAY!

.png)