Japan Digital Payments 2026: What Merchants Need to Know

WRITTEN BY

Dylan Coombs

Citcon

Commercial Leader

Date

May 22, 2026

Subscribe to our interesting updates

SHARE ON

Japan Digital Payments 2026: What Merchants Need to Know

Japan has spent years being labeled a cash-first country that was slowly warming up to digital payments. That story is out of date.

In 2025, Japan's cashless payment ratio reached 58%, total cashless spending hit a record 162.7 trillion yen, and 42.7 million international tourists arrived and spent 9.5 trillion yen while they were there. Every major source market for those tourists, including China, South Korea, Taiwan, and Hong Kong, has its own preferred mobile wallet. Many of those visitors now expect to use it at checkout.

For merchants selling in Japan, selling to Japanese consumers abroad, or trying to capture tourist spend at the point of sale, what matters in 2026 is straightforward: which wallets do your customers use, why do they use them, and how do you accept them all without building a different integration for each one?

This guide answers those questions.

Why the 58% Number Is Different from What You May Have Seen Before

Japan's government recently changed how it calculates the cashless payment ratio. The old method divided cashless spending by total private consumption, which included a statistical concept called "imputed rent." This represents the notional rent that homeowners pay to themselves. Since no one actually pays that with a QR code, it inflated the denominator and made Japan's cashless adoption look smaller than it really was.

The new measure uses a narrower, more practical denominator focused on actual consumer spending. Under that measure, Japan reached 58% in 2025. The government's next target is 65% by 2030.

The practical point for merchants is this: Japan's cashless market is larger and further along than the old headline number suggested.

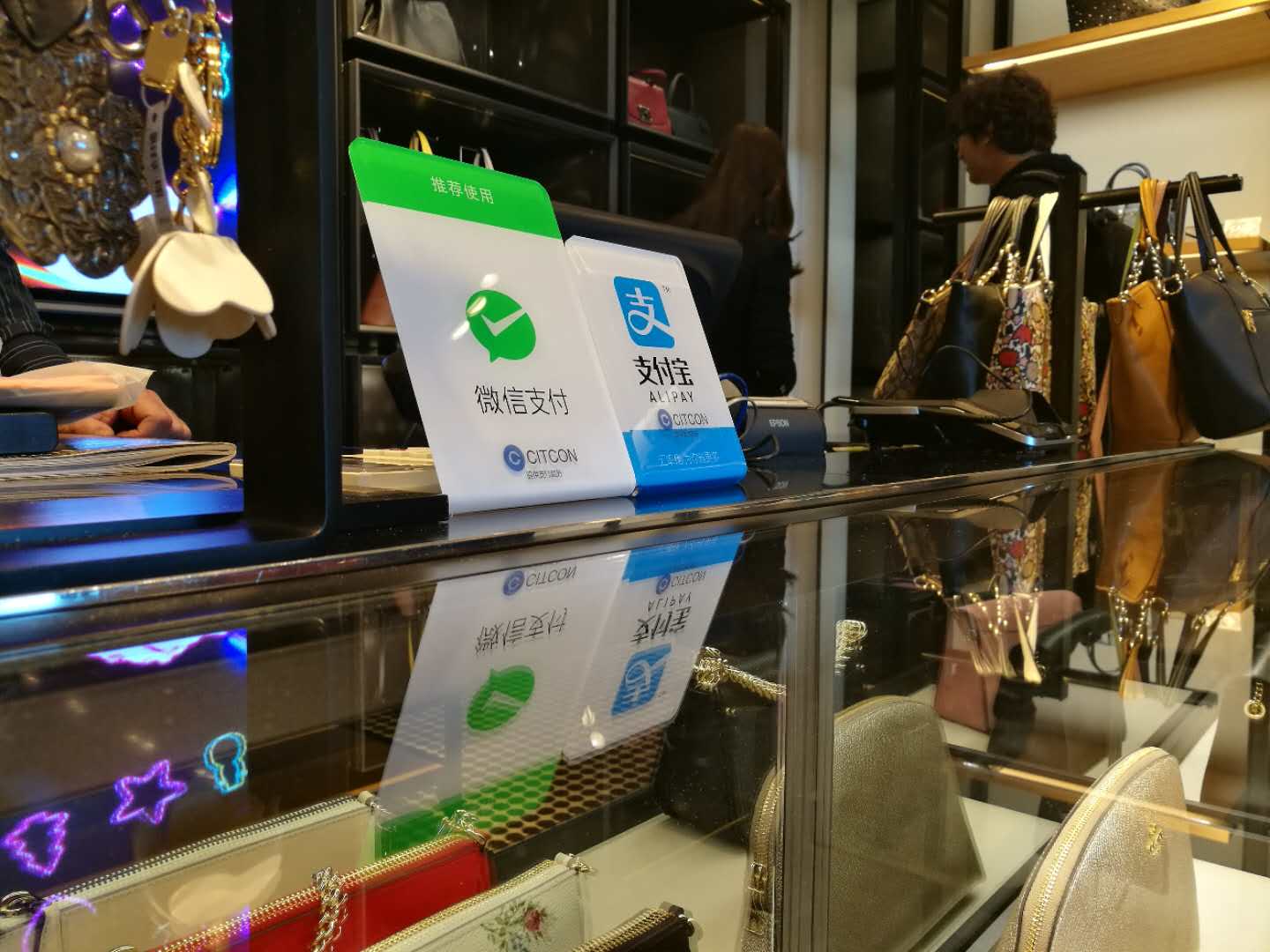

The Wallets That Matter in Japan Right Now

Japan's QR payment market has consolidated significantly. LINE Pay shut down in April 2025, with its users migrating to PayPay. That exit clarified the field. Here is who remains, and why each one matters.

PayPay

PayPay has 72 to 73 million registered users, which is roughly 75% of Japan's smartphone users. About 40 million of them transact every month. The platform processed 12.5 trillion yen in fiscal year 2024 and holds approximately 65% of all QR payment volume in Japan.

PayPay was built to be easy for merchants to adopt. A printed QR code at the register is enough. No expensive terminal, no complicated setup. That simplicity, combined with heavy early promotions, drove the adoption that now makes PayPay the default QR option across more than 4 million merchant locations, from major convenience store chains to small ramen shops.

The platform has expanded well beyond payments. By 2026, PayPay users can also manage a PayPay Bank account, buy and sell stocks, purchase insurance, pay utility bills, and order food delivery without leaving the app. Switching away from PayPay has become genuinely difficult for users who have moved more of their financial life onto the platform.

For inbound tourists, PayPay has also built the largest cross-border acceptance network in Japan. Users of 28 overseas wallets across 14 countries, including Alipay, WeChat Pay, Kakao Pay, Toss, GCash, Touch 'n Go eWallet, TrueMoney, Octopus, and Taishin Pay+, can scan a PayPay QR code and pay in their home currency. For merchants, that single QR code already covers a large share of the tourists walking through their door.

Rakuten Pay

Rakuten Pay is the wallet for consumers who have built their shopping life around the Rakuten ecosystem.

Rakuten is often described as Japan's Amazon, but it is more than that. The Rakuten Group spans e-commerce (Rakuten Ichiba), mobile telecoms (Rakuten Mobile), banking (Rakuten Bank), travel (Rakuten Travel), investing (Rakuten Securities), and insurance. For consumers using several of those services, Rakuten Pay is how they earn and spend Rakuten Points across everything they buy.

Rakuten Points is the most widely used loyalty program in Japan, with 59.3% of consumers enrolled as of a 2024 survey. The program's core mechanic is SPU, which stands for Super Point Up. Using more Rakuten services earns higher point multipliers on purchases. A consumer who shops on Rakuten Ichiba, pays with Rakuten Pay, holds a Rakuten Card, and uses Rakuten Mobile can earn 10 times or more points per purchase compared to someone using only one service.

Rakuten Securities has also introduced the option to invest Rakuten Points directly in stocks. For many younger consumers, it is their first experience with investing, and it deepens the financial relationship with the platform in a way that makes leaving feel costly.

In QR payment market share terms, Rakuten Pay holds 36%, second only to PayPay. For merchants selling on or adjacent to Rakuten Ichiba, accepting Rakuten Pay is not optional. Consumers who can earn points on a purchase will choose the merchant who lets them.

iAEON and AEON Pay

AEON is one of Japan's largest retail groups, covering supermarkets, shopping malls, pharmacies, and general merchandise stores across the country. iAEON is the app that connects all of it.

Launched in 2021, iAEON surpassed 10 million downloads by June 2024. AEON plans to unify over 100 million members, including AEON Card holders and WAON electronic money users, under the iAEON platform. Recent additions include bank-linked payments and the ability to pay entirely with accumulated WAON points.

What makes iAEON significant for merchants is its physical presence. No app-only wallet can replicate the loyalty flywheel of a platform tied to the specific stores a consumer visits multiple times a week. For the household spending segment, particularly families doing regular grocery runs, AEON Pay and WAON points are part of how they think about the cost of every shop.

Expo 2025 Osaka listed AEON Pay as an official accepted QR payment method alongside PayPay, Rakuten Pay, au PAY, d-Barai, and Merpay. Its national profile has grown.

d-Barai, Mobile Suica, and au PAY

Three other platforms deserve a mention because they show up consistently in high-frequency daily spending.

d-Barai is NTT Docomo's payment service. It is linked to d POINT, used by 38.9% of Japanese consumers, and holds 28.6% of QR payment volume. It is most relevant for merchants whose customers are primarily Docomo mobile subscribers.

Mobile Suica and PASMO are transit IC cards, now accessible via Apple Pay and Google Pay on most smartphones. 90% of transit IC cards are available on mobile as of 2025. These cards handle the fastest and most frequent daily transactions: train gates, convenience store counters, vending machines. For merchants in transit-adjacent retail, this is the payment layer that handles most of their volume.

au PAY is KDDI's mobile wallet, linked to Ponta points, which 40.5% of Japanese consumers use. It was listed as an Expo 2025 payment partner and remains relevant among KDDI's subscriber base.

Why Japanese Consumers Pick a Wallet

Understanding which wallets exist is only half of it. The more useful question is why people choose one over another, because the answer shapes how merchants should think about checkout.

In Japan, wallet choice is mostly a loyalty decision.

There is a concept in Japan called poi-katsu, written in Japanese as ポイ活. It refers to the practice of maximizing point earnings on every transaction. It is not a niche habit. Yano Research Institute projects Japan's loyalty point service market will reach 3.28 trillion yen by 2028. Social media accounts dedicated entirely to point maximization have hundreds of thousands of followers.

The core technique is called niju-dori, which means "taking twice." A consumer presents a loyalty card at the register and pays with a wallet that earns its own points on the same transaction. On a single grocery purchase, a Rakuten Pay user at a participating store might earn Rakuten Points on the payment, stack additional store-level points from the retailer's own program, and apply a bonus coupon from the app.

The practical consequence for merchants is this: Japanese consumers do not choose a payment method because it is fast or familiar. They choose the one that earns them the most points at that specific store. The five most-used loyalty programs in Japan by consumer adoption in 2024 were Rakuten Points at 59.3%, T-Point/V-Point at 48.3%, Ponta at 40.5%, d POINT at 38.9%, and PayPay Points at 38.1%.

Wallet selection follows a few consistent patterns:

- Consumers stay where their largest point balance already is, because switching means losing accumulated value

- Regular AEON shoppers gravitate to iAEON because that is where their WAON points build up

- Rakuten Ichiba shoppers gravitate to Rakuten Pay because SPU rewards them for consolidating spend on the platform

- PayPay Points have no expiration date, which is a practical reason many consumers use PayPay as their backup wallet across merchants where their primary loyalty program is not available

For merchants, the takeaway is direct: accepting a wallet also means participating in the loyalty program attached to it. Checkout conversion in Japan is partly a loyalty question.

Japan's Inbound Tourism Opportunity in 2026

Japan received 42.7 million international visitors in 2025, more than at any point in its history. They spent 9.5 trillion yen, up 16.4% from 2024.

Spending by source market:

- China: 2 trillion yen (21.2% of total)

- Taiwan: 1.2 trillion yen (12.8%)

- United States: 1.1 trillion yen (11.9%)

- South Korea: 986 billion yen (10.4%)

- Hong Kong: 561 billion yen (5.9%)

Each of those source markets has dominant home wallets. Chinese tourists use Alipay and WeChat Pay. Korean tourists use Kakao Pay, Naver Pay, and Toss. Taiwanese tourists use Taishin Pay+ and other local options. Hong Kong tourists use Octopus and AlipayHK.

Through PayPay's partnerships with Alipay+ and the HIVEX network, users of 28 overseas wallets can already scan a PayPay QR code at any enrolled merchant in Japan and pay in their home currency. The currency conversion happens automatically. The merchant settles in yen.

The commercial impact is real. At Daimaru Matsuzakaya department stores, transaction volume from Alipay+ partner wallets rose more than 10 times year-on-year in early 2024. In Asakusa, cross-border mobile transaction volume runs more than 5 times the average for other merchants in the area.

Japan's Tourism Agency has set a target of 15 trillion yen in inbound spending by 2030. The merchants who capture more of that growth will be the ones whose checkout already works for the tourist walking in the door.

Three Payment Trends Shaping Japan in 2026

Beyond wallet rankings, three shifts are changing how payment infrastructure works in Japan right now.

NFC contactless is expanding fast. Japan's NFC payments market is growing at an 11.83% annual rate through 2033. Over half of newly issued cards in Japan are now contactless. Apple's launch of Tap to Pay in Japan in 2024, supported by domestic partners including GMO Financial Gate, opened iPhone-based contactless acceptance to merchants who previously had no compatible hardware. Combined with Suica and PASMO's FeliCa-based tap infrastructure, tap-to-pay is becoming the secondary checkout standard alongside QR codes, not a replacement for them but an increasingly expected option.

Government policy is pushing harder. METI updated its Credit Card Security Guidelines in March 2025 and has set a 65% cashless target by 2030 under the revised domestic measure. Digital salary payment rules now allow wages to be transferred directly into registered digital wallets. The direction of travel is clear and the pace is picking up.

The wallet field is narrowing. The LINE Pay exit in April 2025 was not an isolated event. It reflected a broader trend: platforms that cannot offer a range of financial services beyond payments will find it harder to retain users. PayPay now offers banking, investment, insurance, and peer-to-peer transfers. Rakuten Pay is backed by a group that covers telecoms, travel, and stock trading. Platforms competing on payment convenience alone face an increasingly difficult position. For merchants, this means fewer integrations will cover more of the market than they did three years ago.

How Citcon Helps Merchants Accept Japan's Wallets

Knowing which wallets matter is the research problem. Actually accepting them is the operational one.

Most businesses cannot build separate integrations for PayPay, Rakuten Pay, Alipay, WeChat Pay, and UnionPay and then maintain them all while also managing card payments, currency conversion, and fraud protection across markets. The engineering cost alone makes it impractical.

Citcon solves this with a single integration that covers more than 100 wallets, credit cards, and local payment methods across online, in-store, and mobile channels.

For Japan, Citcon accepts:

- PayPay — 72 to 73 million registered users, roughly 65% of Japan's QR payment volume

- Rakuten Pay — second-largest QR wallet at 36% market share, deep integration with Japan's dominant e-commerce platform

- Alipay — the primary wallet for Chinese tourists, who spent 2 trillion yen in Japan in 2025

- WeChat Pay — widely used by Chinese consumers for both in-store and online purchases

- UnionPay — covers more than 9 billion cards globally and is commonly used by tourists across East Asia

- JKO Pay and additional APAC wallets through Citcon's regional coverage

In August 2025, Citcon expanded its Japan infrastructure through a partnership with GMO Payment Gateway, one of Japan's leading domestic payment processors and a prior investor in Citcon. That partnership added GMO's full suite of Japanese payment methods to Citcon's platform, including domestic credit cards, local digital wallets, and convenience store payments, known in Japan as konbini payments. Konbini payments let consumers pay for online orders in cash at 7-Eleven, Lawson, or FamilyMart, and remain important for the segment of Japanese shoppers who still prefer to handle certain transactions that way.

As a result of that partnership, merchants in the U.S., Canada, U.K., and China can now accept Japanese payment methods through Citcon. Japanese merchants can use Citcon's global infrastructure to accept international payments from buyers in other markets. All transactions route through local acquirers in Japan, which reduces processing costs and improves the rate at which payments are approved.

"This partnership with GMO-PG adds essential Japanese payment methods to our platform, enabling our merchants across North America, Europe, and Asia to better serve Japanese customers. It also allows GMO to bring Citcon's global capabilities to its domestic merchants, creating a powerful two-way bridge for commerce." Casey Bullock, CEO, Citcon.

Japan Payments FAQ

What is Japan's cashless payment ratio in 2026? Under METI's revised domestic spending measure, Japan reached 58% in 2025. The government targets 65% under that same measure by 2030. The older metric, which used a broader denominator, showed 42.8% for 2024.

Which wallet has the most users in Japan? PayPay, with 72 to 73 million registered users and around 40 million people using it every month. It holds roughly 65% of QR code payment volume in Japan.

Can international tourists use their home wallets in Japan? Yes. Through PayPay's partnerships with Alipay+ and the HIVEX network, users of 28 overseas wallets from 14 countries, including Alipay, WeChat Pay, Kakao Pay, Toss, GCash, Touch 'n Go eWallet, TrueMoney, Octopus, and Taishin Pay+, can pay at any PayPay-enrolled merchant across Japan.

What is poi-katsu and why should merchants care? Poi-katsu is the Japanese practice of maximizing loyalty point earnings on every purchase. Japanese consumers regularly choose where to shop and how to pay based on which option earns the most points in that context. Merchants that accept the wallet tied to a customer's main loyalty program see higher checkout conversion as a result.

What is konbini payment? Konbini payment lets consumers pay for online orders in cash at convenience stores like 7-Eleven, Lawson, and FamilyMart. It is still used by a meaningful share of Japanese consumers for online purchases and is part of Citcon's Japan payment stack through the GMO Payment Gateway partnership.

How does a foreign merchant start accepting Japanese wallets? Through Citcon, merchants can accept PayPay, Rakuten Pay, Alipay, WeChat Pay, UnionPay, konbini payments, and more, whether online or in-store, through a single integration. Talk to Citcon to get started.

What to Take Away from Japan's Payment Market in 2026

Japan is past the tipping point. The cashless infrastructure is in place, consumer behavior has shifted permanently across age groups, and inbound tourism is at record levels with no sign of slowing. The question now is not whether Japan's digital payment market is real. It is whether your business is set up to participate in it.

The wallets that matter most, PayPay, Rakuten Pay, and iAEON, are not really competing on technology. They are competing on ecosystem depth. PayPay wins because it is everywhere and handles more than just payments. Rakuten Pay wins because it sits inside the loyalty program that 59% of Japanese consumers already use. iAEON wins because it is tied to the grocery store and shopping mall where millions of Japanese households spend money every week.

Merchants that accept those wallets are included in those ecosystems. Merchants that do not are simply absent from the checkout consideration for a large part of the market.

Citcon makes it practical to be present across all of them without rebuilding your payment infrastructure from scratch.

Japan's payment market is open and growing. The practical next step is making sure your checkout reflects that.

Talk to Citcon about accepting Japan's top wallets

.jpg)

.png)