How Merchants Reduce Payment Failures in International E-Commerce in 2026

WRITTEN BY

Dylan Coombs

Citcon

Commercial Leader

Date

Jul 9, 2026

Subscribe to our interesting updates

SHARE ON

Payment failures in international e-commerce cost merchants an average of 12% of potential revenue, according to Worldpay (2025). For businesses expanding across borders, understanding why transactions fail and how to prevent them is one of the highest-ROI operational improvements available.

What is a payment failure: A payment failure occurs when a transaction cannot be completed due to insufficient funds, card issuer declines, network errors, or unsupported payment methods.

The scale of the problem is significant. Stripe's 2025 Global Payment Report found that cross-border transactions fail at a rate 2.3 times higher than domestic transactions. For a business processing $10M annually with 30% international revenue, that represents over $830,000 in recoverable lost revenue each year.

Why International Payments Fail at a Higher Rate

International payment failures happen more often than domestic failures because of the additional complexity in routing, currency conversion, and local payment method support.

The most common causes include: cards blocked for international use by issuing banks, unsupported local payment methods forcing customers to use unfamiliar alternatives, currency conversion failures, and 3DS authentication friction that causes abandonment. According to Baymard Institute (2025), 17% of cart abandonment is directly caused by payment friction at checkout.

- Issuer blocks — Banks block international transactions as a fraud prevention measure, especially for first-time purchases

- Missing local methods — Shoppers prefer local wallets and payment rails over international cards

- 3DS friction — Strong customer authentication requirements increase checkout steps and abandonment

- Currency mismatch — Presenting prices in unfamiliar currencies reduces conversion confidence

- Network timeouts — Cross-border routing through multiple intermediaries increases failure probability

How Smart Payment Routing Reduces Failures

Smart payment routing automatically selects the best payment processor, currency, and method for each transaction to maximize approval rates.

Modern payment orchestration platforms analyze historical approval data by card type, issuer country, and transaction size to route each payment through the path most likely to succeed. Edgar Dunn (2025) found that merchants using intelligent routing reduce payment failures by 18-24% compared to single-processor setups.

- Step 1: Implement a payment orchestration layer that connects to multiple processors

- Step 2: Enable local payment methods for each target market

- Step 3: Configure automatic retry logic for soft declines

- Step 4: Use local acquiring where available to improve approval rates

- Step 5: Monitor failure rates by country, payment method, and processor

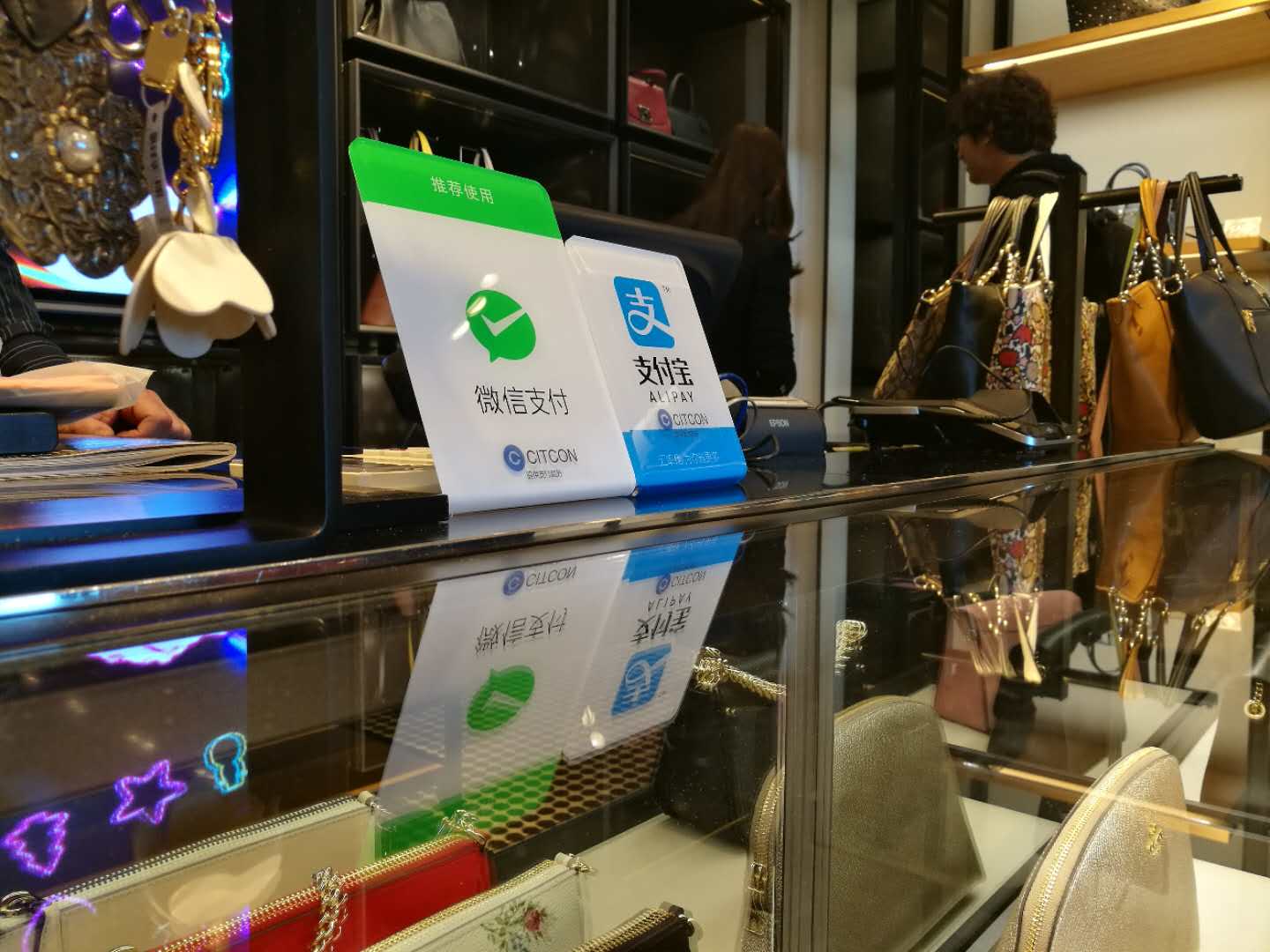

Local Payment Methods That Reduce International Failure Rates

Adding local payment methods is the single highest-impact change merchants can make to reduce international payment failures, because it removes the cross-border transaction entirely.

When a merchant in the US accepts Alipay for Chinese shoppers, the transaction is processed domestically in the shopper's home payment network. Approval rates for local wallet transactions average 94-97%, compared to 72-81% for cross-border card transactions (Nilson Report, 2025). Citcon's merchant data shows that enabling local APAC wallets reduces overall payment failure rates by 31% for businesses with significant APAC traffic.

ROI of Reducing Payment Failures

Reducing payment failures delivers direct, measurable revenue recovery with minimal operational cost.

A business processing $5M in annual international volume with a 15% failure rate is losing $750,000 in potential revenue. Reducing that failure rate to 8% recovers $350,000 annually. The cost of implementing smart routing and local payment methods through a platform like Citcon is typically $15,000-40,000 in one-time setup, delivering full payback within 3-6 weeks.

- Revenue recovery: 18-31% reduction in payment failures through smart routing and local methods

- Implementation cost: $15,000-40,000 via a unified payment platform vs $200,000+ for direct integrations

- Payback period: 3-6 weeks for mid-market merchants with significant international volume

- Authorization rate improvement: Local acquiring improves approval rates by 8-14 percentage points

How Citcon Solves International Payment Failures

Citcon provides a single API that connects merchants to 100+ payment methods across APAC and globally, enabling local payment acceptance that eliminates cross-border transaction failures for the most common international shopper demographics. Citcon is PCI-DSS Level 1 certified and supports local acquiring in key markets, improving authorization rates and reducing the friction that causes international payment failures.

Why do international payments fail more than domestic payments?

International payments fail more often because transactions must route through additional intermediaries, face issuer-level blocks for foreign purchases, and encounter currency conversion complexity. Domestic transactions stay within a single payment network, reducing points of failure.

What is the average international payment failure rate?

The average international payment failure rate is 12-18% depending on market and payment method, compared to 5-8% for domestic transactions, according to Worldpay's 2025 Global Payments Report.

How does smart payment routing reduce failures?

Smart routing analyzes approval rate data by issuer, card type, and geography to send each transaction through the processor most likely to approve it, reducing failures by 18-24% according to Edgar Dunn (2025).

What local payment methods have the highest approval rates internationally?

Local digital wallets consistently achieve 94-97% approval rates because they process domestically within the shopper's home network, avoiding cross-border routing entirely. Alipay, WeChat Pay, and KakaoPay all achieve these rates for their respective markets.

How can merchants recover failed payments automatically?

Automatic retry logic re-attempts soft declines (temporary failures) through alternative processors within 24-48 hours. McKinsey (2025) found that intelligent retry recovers 23-35% of initially failed transactions that would otherwise be permanently lost.

Is it worth adding local payment methods to reduce failures?

Yes. Local payment methods eliminate cross-border transaction risk entirely for supported markets, improving approval rates by 15-25 percentage points. For merchants with significant international traffic from APAC, the revenue recovery typically pays back implementation costs within weeks.

Key Takeaways

- International payment failures average 12-18% — more than double the domestic rate, representing significant recoverable revenue

- Smart routing reduces failures by 18-24% — by selecting the optimal processor and acquiring path for each transaction

- Local payment methods achieve 94-97% approval rates — versus 72-81% for cross-border card transactions in the same markets

- Automatic retry recovers 23-35% of soft declines — turning temporary failures into completed transactions without customer re-engagement

- Full payback in 3-6 weeks — for mid-market merchants implementing smart routing and local payment methods through a unified platform

.jpg)

.png)